Does a company without shareholder equity have value? Often, if you’re dealing with a bad or fair company, you’d have to be careful if you’re considering investing in one like that. Some companies, however, and those are often of a higher quality than other companies, can operate today without a positive shareholder equity.

If a company is gushing free cash flow, and it has no problems of servicing its debts, indeed the company can be quite valuable, even if the stock has a negative equity. There’s nothing magical about the stock equity being positive or negative says Warren Buffett in the video below in this post.

If you ask me, it would make sense to look at the company’s earning power compared to its enterprise value when valuing the company and its free cash flow. Read more on what enterprise value is here.

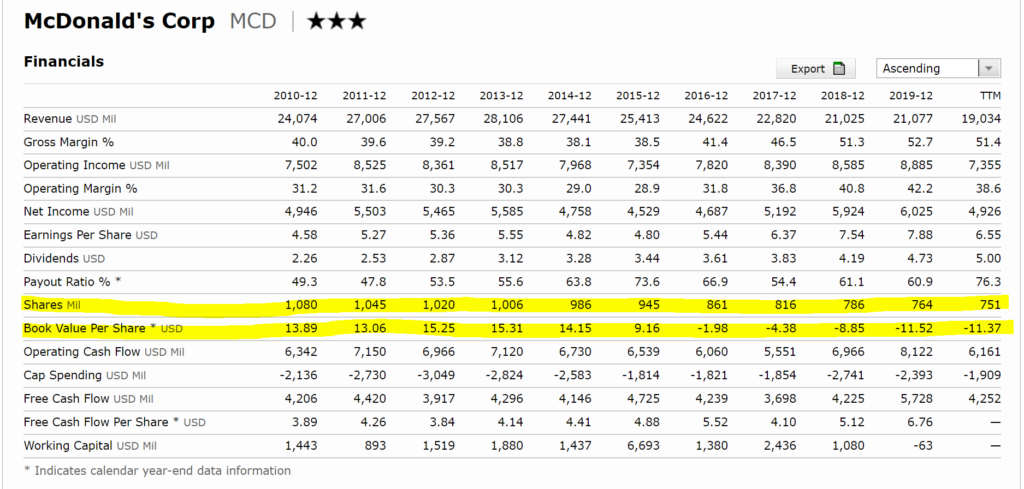

Look at McDonald’s for example. Its equity or book value per share is close to -$11. It started the decade with around a positive $14. As you see in the table below the company is gushing free cash flow, eventhough it has not shown a growth of revenue or operating income over the last ten years.

Take a look at the two rows highlighted in yellow. You see that the amount of shares outstanding have decreased from about 1 billion to 751 million over the decade. While still paying a growing annual dividend, the company has been buying back shares with its remaining free cash flow.

The main cash movements over the last ten years have been the following at McDonalds Corporation. You can follow by looking at the highlighted rows in the table below.

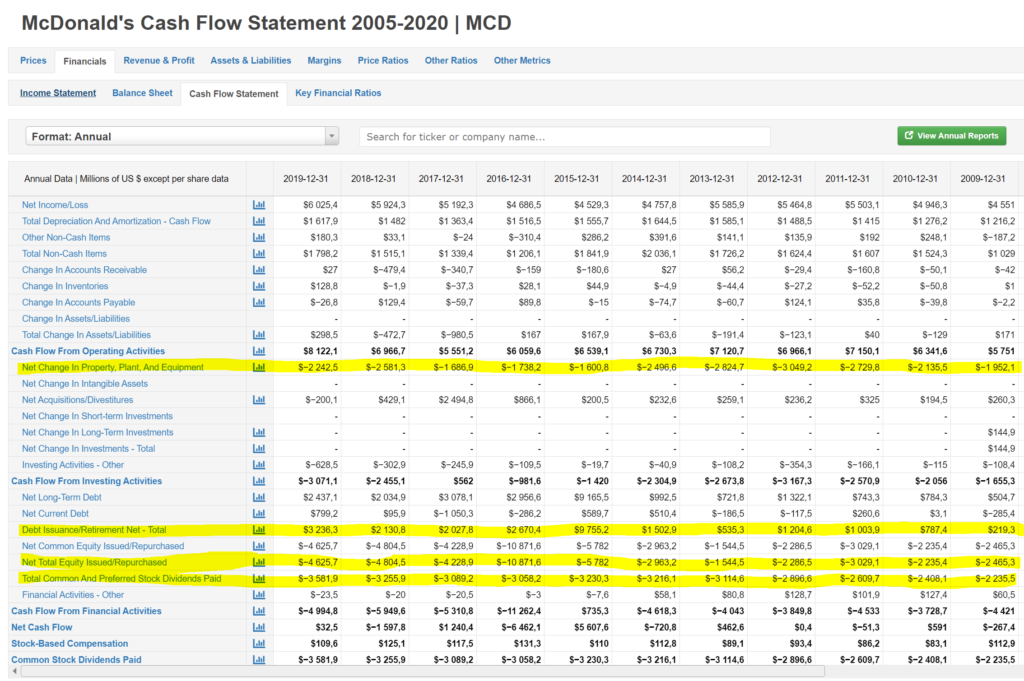

On average its management has spent about $2bn in buying new assets for its operations. That comprises of cash flow mainly for new restaurants and real estate for the restaurants to operate in, as well as maintenance of the exisiting ones.

Looking at the history from the figures below, every year the company management has issued more and more debt even though the company has been earning more operating cash flow than has been paid out for its assets aquisitions and dividends. It has used all of this increase of debt and more to do buyback of shares. It has not been building up free cash on its balance sheet.

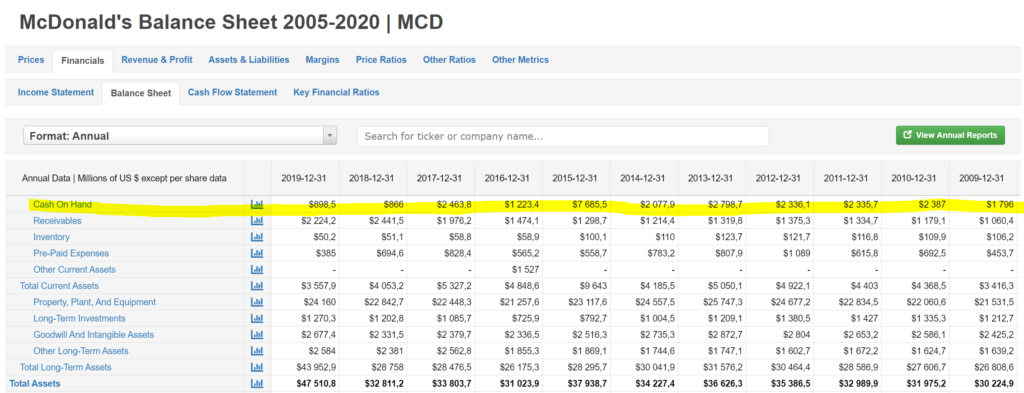

We see from the balance statement that after the company’s capital allocation has been done; buying and maintaining new assets, paying a dividend, buying back shares and issuing new debt, the company has not been piling up any cash on the side. The cash balance has gone from about $2bn ten years ago to less than $1bn at the end of 2019.

The company has bought back over $40bn of shares in itself, while it has borrowed and extra $25bn over the decade.

Does McDonald’s shares still have value?

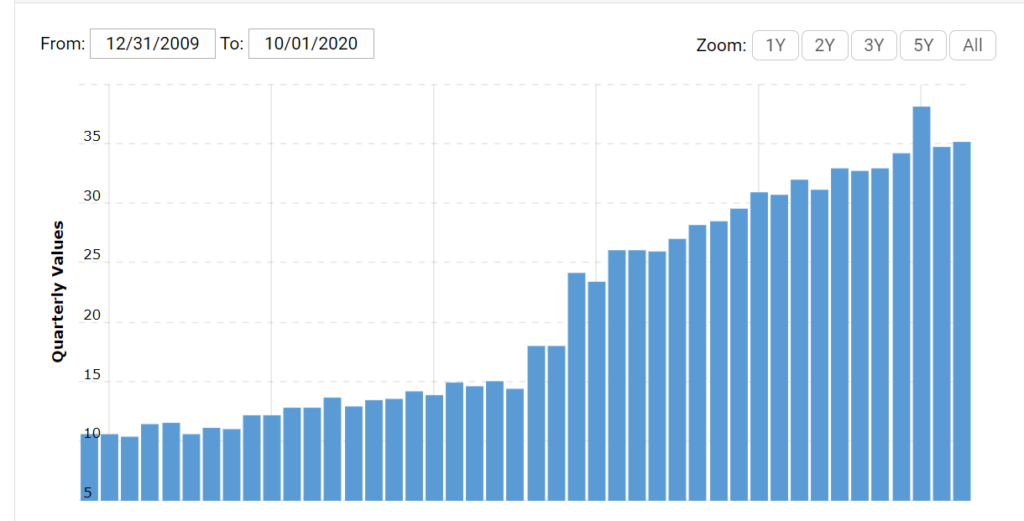

Certainly the stock market thinks so. It has been bidding the share price up quite consitently over the last ten years. The current negative book value per share of -$11 does not seem to bother the stock market, which has been trading the stock between about $140 and $230 over the last year.

Points to consider when valuing the company

If I were to buy McDonalds stock these are few of the things I’d check.

- Is it a wonderful company?

- It has a great brand, customers love it, and it owns prime real estate with a very respectable sales per square feet (or square meters).

- It generates a very high return on assets

- One indicator to use is that it’s return on assets is very high, north of 10-15 percent. Return on equity would be negative here, because of the negative equity.

- Does the company gush free cash flow?

- As you see from the first table above, the company has been producing an average free cash flow of about $4bn per year.

- What is the earning power of the business?

- It seems to my knowledge that the restaurant real estate business of McDonalds is capable of returning at least 10 to 15 percent on its assets on the balance sheet. And its operating cash flow should be able to grow from $7-8bn now.

- If I regard McDonald’s as a real estate company, do I have other alternatives of investing that would give me a higher return on capital?

- Will the cash flow be able to grow the next ten years?

- It has not been growing very much over the last years. Will that change?

- What is the current valuation compared to its cash flow?

- The current enterprise value of McDonald’s is $195 bn. I’d have to take a close look on what my actual free cash flow in terms of owner’s earnings would be. Let’s say for simplicity’s sake that it is about $7bn yearly. Would I be happy with the current stock price? The current stock price gives the company an enterprice value of $195 bn. That means I’d only get about 3.6% if I were to buy the whole business, when I’m comparing my owner’s earnings to the amount of cash needed to buy the whole business.

- I’d be much more happier to buy it at an enterprise value of $120 bn in 2015 with about the same amount of owner’s earnings.

Conclusion

McDonald’s will be on my watchlist, but at the current stock price and ratio of owner’s earnings to enterprise value, I’m waiting for a fall in price before the stock would be more interesting.